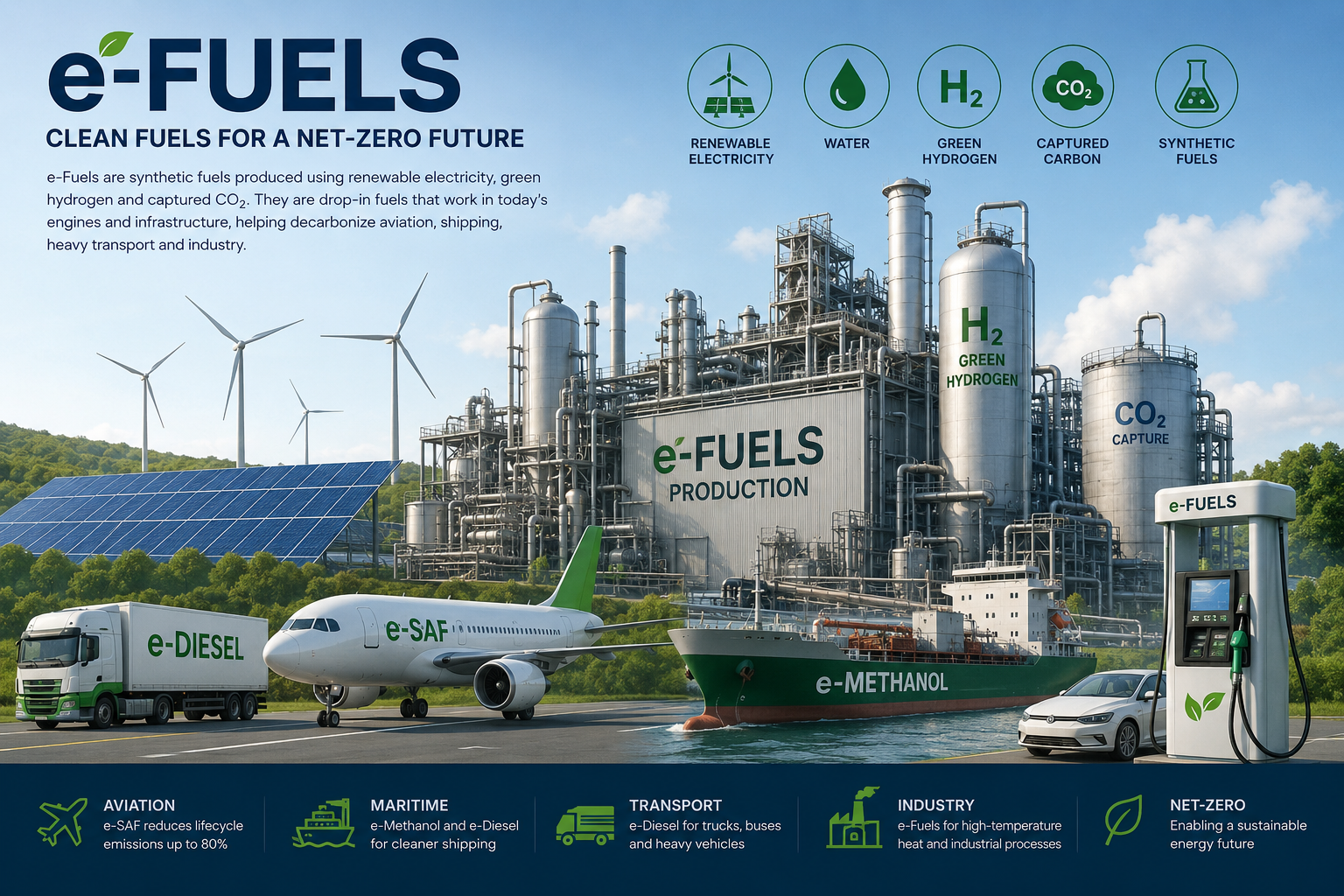

RED III Establishes Renewable Electricity Requirements for e-Fuel Certification

The Renewable Energy Directive III framework mandates that electro-synthetic aviation fuel must be produced using 100% renewable electricity to qualify for sustainability certification under EU law. This requirement directly impacts Power-to-Liquid facilities seeking to claim eSAF as renewable fuel of non-biological origin, compelling project developers to secure dedicated renewable energy contracts or demonstrate additionality through grid connections verified against strict temporal and geographical correlation criteria. The directive’s lifecycle emissions methodology excludes e-fuels produced with grid electricity unless operators can prove incremental renewable capacity addition.

Certification pathways under RED III now require comprehensive supply chain transparency, from hydrogen production through carbon capture sourcing and final fuel synthesis. Early data from UK SAF mandate implementation shows uncertainty around meeting first-year targets, highlighting how policy design details—including grace periods, penalty structures, and verification protocols—determine whether mandates accelerate or constrain market development. The Boeing-Norsk e-Fuel partnership expansion announced April 15, 2026, reflects industry confidence that regulatory clarity on renewable electricity sourcing will enable commercial-scale eSAF production by 2030.

ReFuelEU Aviation Mandates Create Binding Blending Requirements Across Member States

The ReFuelEU Aviation regulation establishes progressive blending mandates that require aviation fuel suppliers to incorporate minimum sustainable fuel percentages at EU airports, with sub-targets specifically designated for synthetic fuels produced via Power-to-Liquid pathways. These mandates create guaranteed demand that reduces market risk for e-fuel facilities, though implementation challenges remain around feedstock availability, infrastructure readiness, and cost competitiveness relative to conventional jet fuel. The framework includes penalty mechanisms for non-compliance that effectively function as price floors supporting eSAF economic viability during scale-up phases.

Policy shifts around recognition of different carbon capture sources—whether direct air capture, industrial point sources, or biogenic CO2—continue to affect project economics and strategic positioning. The sustainable fuels expected to reach flights by 2026 will operate within this evolving regulatory environment, where certification requirements determine market access and mandate compliance drives procurement decisions across European aviation networks.

Policy Certainty Emerges as Primary Driver for Investment Capital Allocation

Investment flows into e-fuel facilities now depend primarily on policy stability rather than technology readiness, with project financing contingent on long-term regulatory visibility around mandate trajectories, support mechanisms, and certification pathways. The convergence of RED III sustainability criteria with ReFuelEU Aviation blending requirements creates a unified framework that enables financial institutions to model revenue streams and regulatory compliance costs over project lifetimes. Recent developments including federal support updates from entities like the US Department of Energy demonstrate how government backing shapes market development trajectories beyond European borders, though EU policy remains the most prescriptive and binding framework globally for e-fuel commercialization.

Sources

- Boeing and Norsk e-Fuel expand efforts to advance e-fuels

- Early data shows uncertainty that UK SAF mandate can be met in its first year – GreenAir News

- What is eSAF | News and views | Air bp

- Sustainable Fuels Expected to Reach Pumps, Fleets, and Flights by 2026

Featured image via Unsplash.