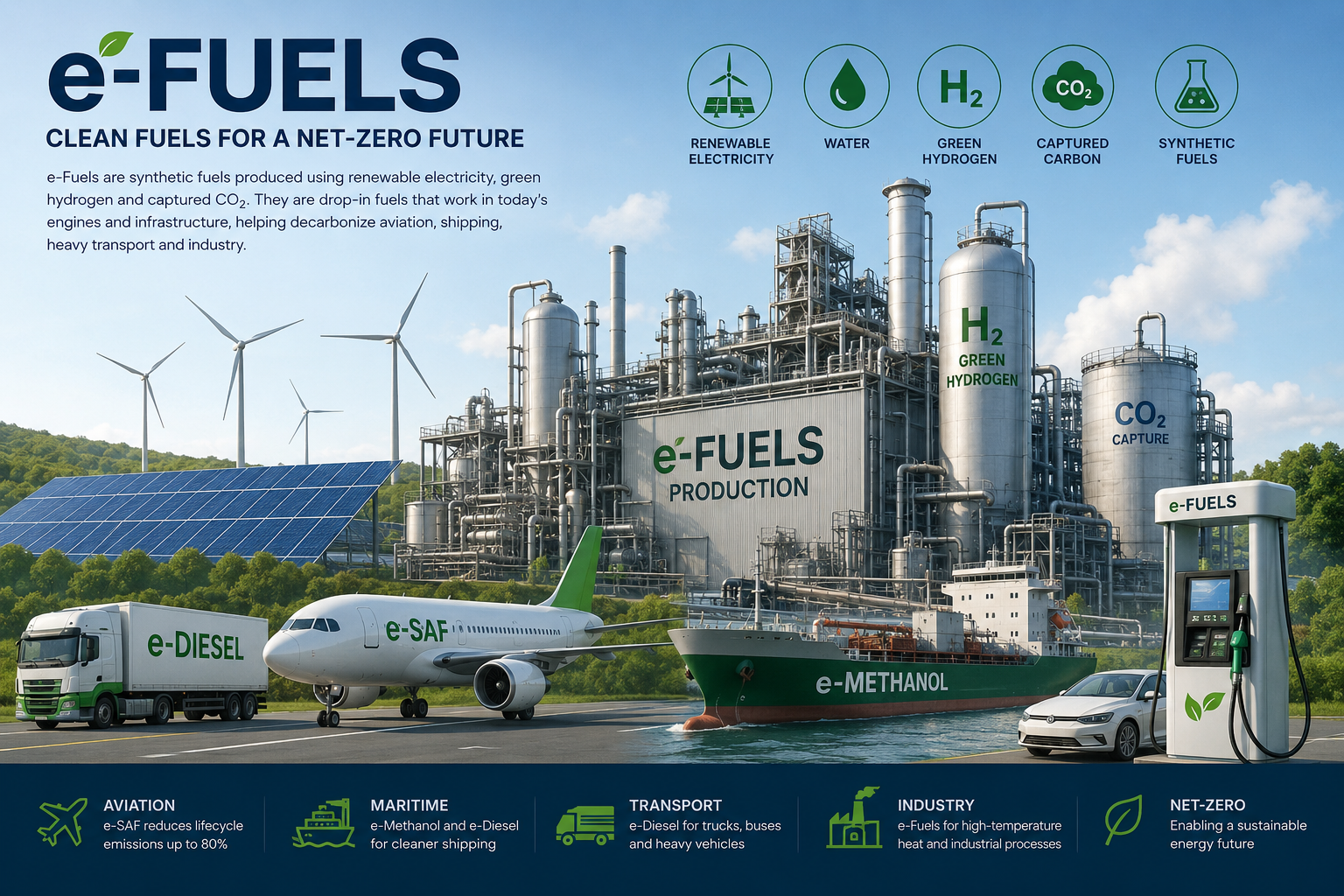

ReFuelEU Aviation Certification Frameworks Accelerate Under Mandate Pressure

The European Union’s ReFuelEU Aviation regulation imposes legally binding SAF blending quotas that climb from 2% in 2025 to 70% by 2050, with intermediate targets of 6% in 2030 and 20% in 2035. Certification under the Renewable Energy Directive III (RED III) determines which production pathways qualify for mandate compliance, creating a critical gating function for project viability. LanzaJet’s closure of a $135 million equity round in February 2026 underscores investor confidence in alcohol-to-jet pathways already certified under ASTM D7566, while SkyNRG’s achievement of financial close on its DSL-01 plant in the Netherlands demonstrates that hydroprocessed esters and fatty acids (HEFA) routes retain regulatory certainty.

Certification timelines are now the defining variable in project economics. Patagonia’s $2.5 billion eSAF project, announced in February 2026 as the largest aviation e-fuel initiative globally, faces a dual certification challenge: proving both the renewable origin of input electricity under RED III’s additionality criteria and demonstrating Fischer-Tropsch synthetic paraffinic kerosene (FT-SPK) compliance with ASTM specifications. Industry analysts note that while HEFA pathways benefit from established certification frameworks, Power-to-Liquid e-fuels require novel verification protocols for lifecycle greenhouse gas accounting, particularly for direct air capture CO₂ inputs.

Operational Compliance: Norwegian’s 40% Blend Sets New Benchmark

Norwegian’s launch of a permanent 40% SAF blend on its Aalborg-Copenhagen route in March 2026 represents a twentyfold increase over current EU mandate minimums, positioning the carrier as a testbed for compliance strategies beyond regulatory floors. The route’s daily operations provide real-world data on fuel performance, supply-chain logistics, and mass-balance accounting under the EU’s Union Database for Biofuels—critical inputs for refining certification rules as blending mandates rise. The airline’s decision to source certified SAF rather than wait for lower-cost e-fuels reflects the regulatory premium on established pathways with proven sustainability certification.

This operational milestone also highlights tensions within RED III’s cascading use provisions, which prioritize waste feedstocks over energy crops. As demand for certified SAF outpaces supply from used cooking oil and animal fats, certification authorities face pressure to expand eligible feedstock categories while maintaining lifecycle emission thresholds below the 70% reduction mandate relative to fossil jet fuel.

Investment Flows Follow Regulatory Clarity on E-Fuel Certification

The $2.5 billion scale of Patagonia’s eSAF project and LanzaJet’s ability to raise $135 million in early 2026 signal that capital markets are pricing in eventual certification approval for next-generation pathways. However, these investments carry regulatory risk premiums tied to unresolved questions around renewable electricity additionality criteria and carbon-accounting methodologies for synthetic fuels. SkyNRG’s DSL-01 plant, by contrast, benefits from HEFA pathway maturity but faces feedstock availability constraints as certification rules limit the use of palm oil and other high-indirect-land-use-change materials. The interplay between mandate ambition and certification bottlenecks will determine whether the EU meets its 2030 target of 6% SAF uptake or faces supply shortfalls that trigger compliance cost spikes for airlines.

Sources

- Liquid e-fuels for a sustainable future: A comprehensive review of production, regulation, and technological innovation

- Beyond fossil: the synthetic fuel surge for a green-energy resurgence

- Renewable synthetic fuels: Research progress and development trends

Featured image via Unsplash.