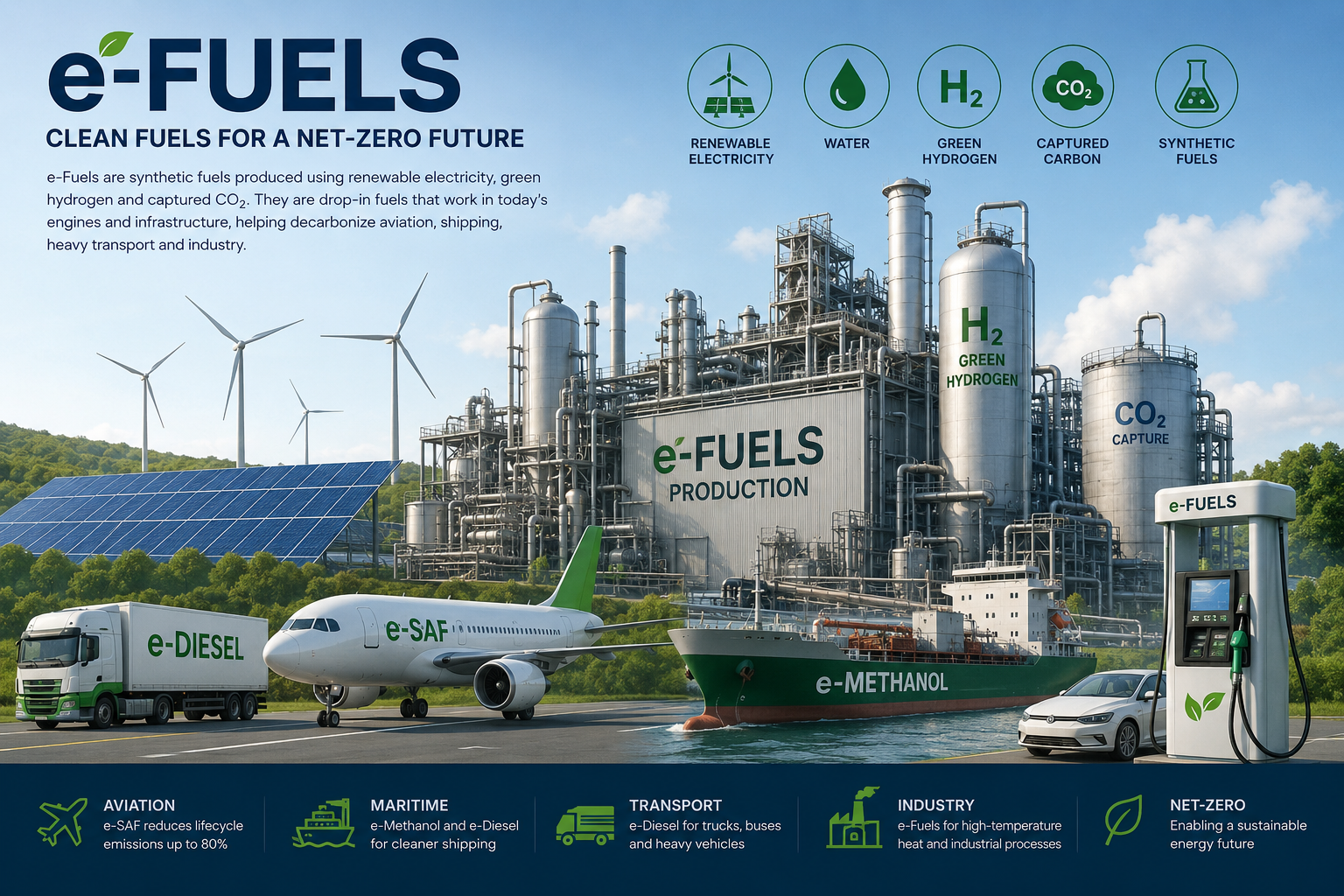

The sustainable aviation fuel sector faces a critical policy-reality gap as European mandates approach and US production scales up. Scandinavian Airlines has issued warnings about potential fuel shortages in Europe, even as American projects secure major financing and rising conventional fuel prices improve the economic case for synthetic alternatives. The developments highlight growing tension between aggressive decarbonization timelines and the infrastructure required to meet them.

SAS Group raised alarms in early May 2026 about Europe’s ability to meet its 2030 sustainable fuel obligations, warning that supply is falling dangerously behind regulatory requirements. The European Union’s mandates require airlines to blend increasing percentages of SAF into conventional jet fuel, but production capacity has not kept pace with policy ambitions. The airline’s concerns reflect broader industry anxiety that fuel availability could become a bottleneck for compliance, potentially forcing operational disruptions or requiring emergency policy adjustments as the deadline approaches.

Across the Atlantic, Green Sky Capital secured financing for a major SAF facility in Egypt, signaling continued investment momentum in the sector despite supply concerns. The Bloomberg-reported project represents a strategic effort to diversify airline energy sources across regions. Meanwhile, Gevo’s patent award for alcohol-to-jet catalyst technology demonstrates ongoing innovation in Power-to-Liquid pathways. These American advances contrast with European warnings, suggesting uneven geographic development in the global SAF infrastructure needed to support international aviation decarbonization goals.

The economics of synthetic fuel production received an unexpected boost as conventional oil prices surged in early May 2026. Climate Change News reported that e-SAF producers now see improved competitive positioning as the price gap between synthetic and petroleum-based jet fuel narrows. This development could accelerate investment in Power-to-Liquid facilities, though the timing remains uncertain for whether new capacity can come online quickly enough to prevent the European shortage that SAS has forecast. The oil price factor adds a market-driven dimension to policy discussions previously focused primarily on mandates and subsidies.

The sustainable aviation fuel sector stands at a policy crossroads where regulatory ambition confronts infrastructure reality. European shortage warnings and American project financing illustrate the uneven global rollout of SAF capacity, while improved economics from conventional fuel price increases offer hope for accelerated deployment. Policymakers in both the EU and US face pressure to either adjust mandate timelines to match realistic production curves or significantly increase support for rapid capacity expansion. The next 18 months will prove critical in determining whether current policies drive transformation or trigger a compliance crisis.